Week 2, Session 5 — Time series basics

Course 3 — #courses

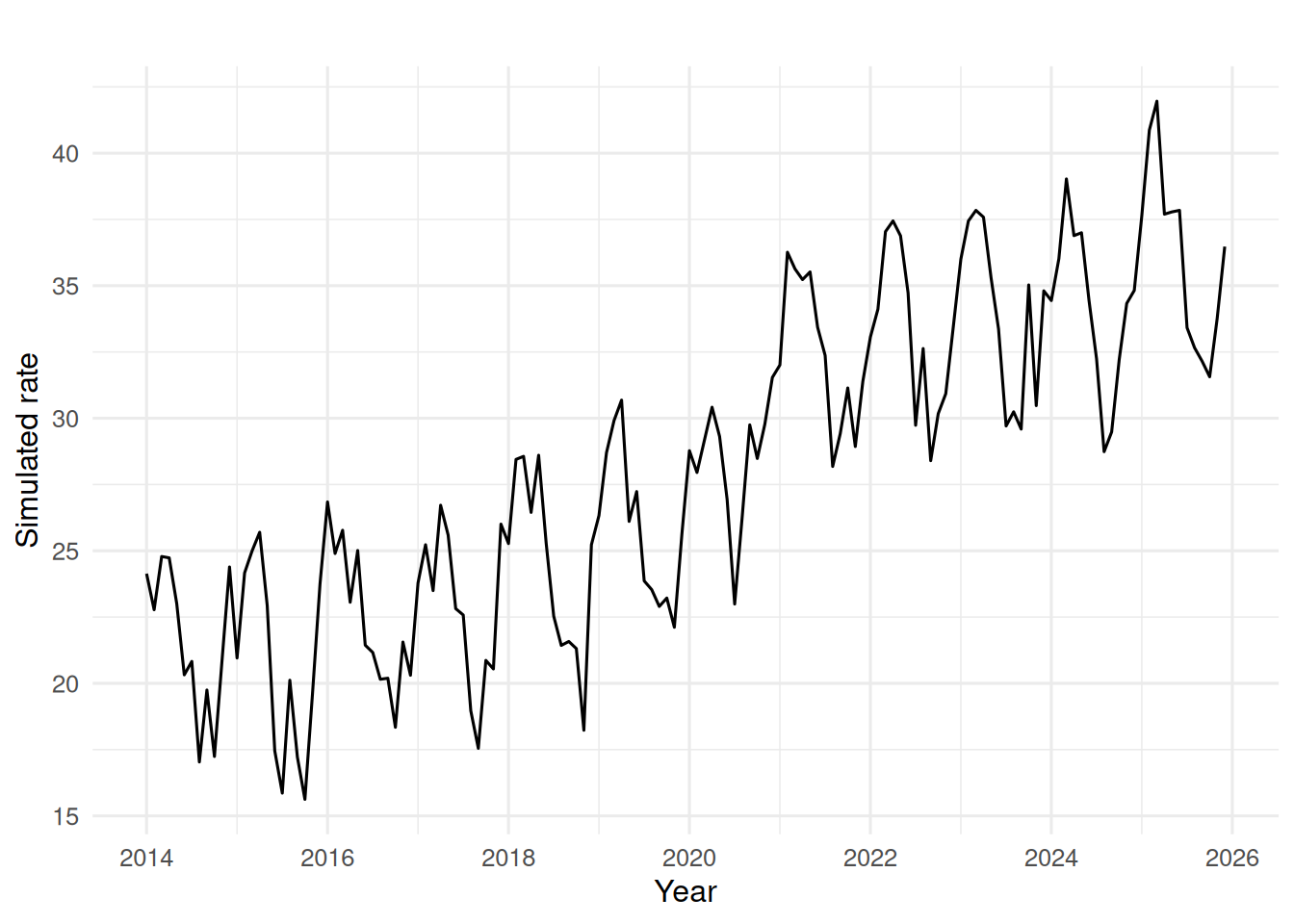

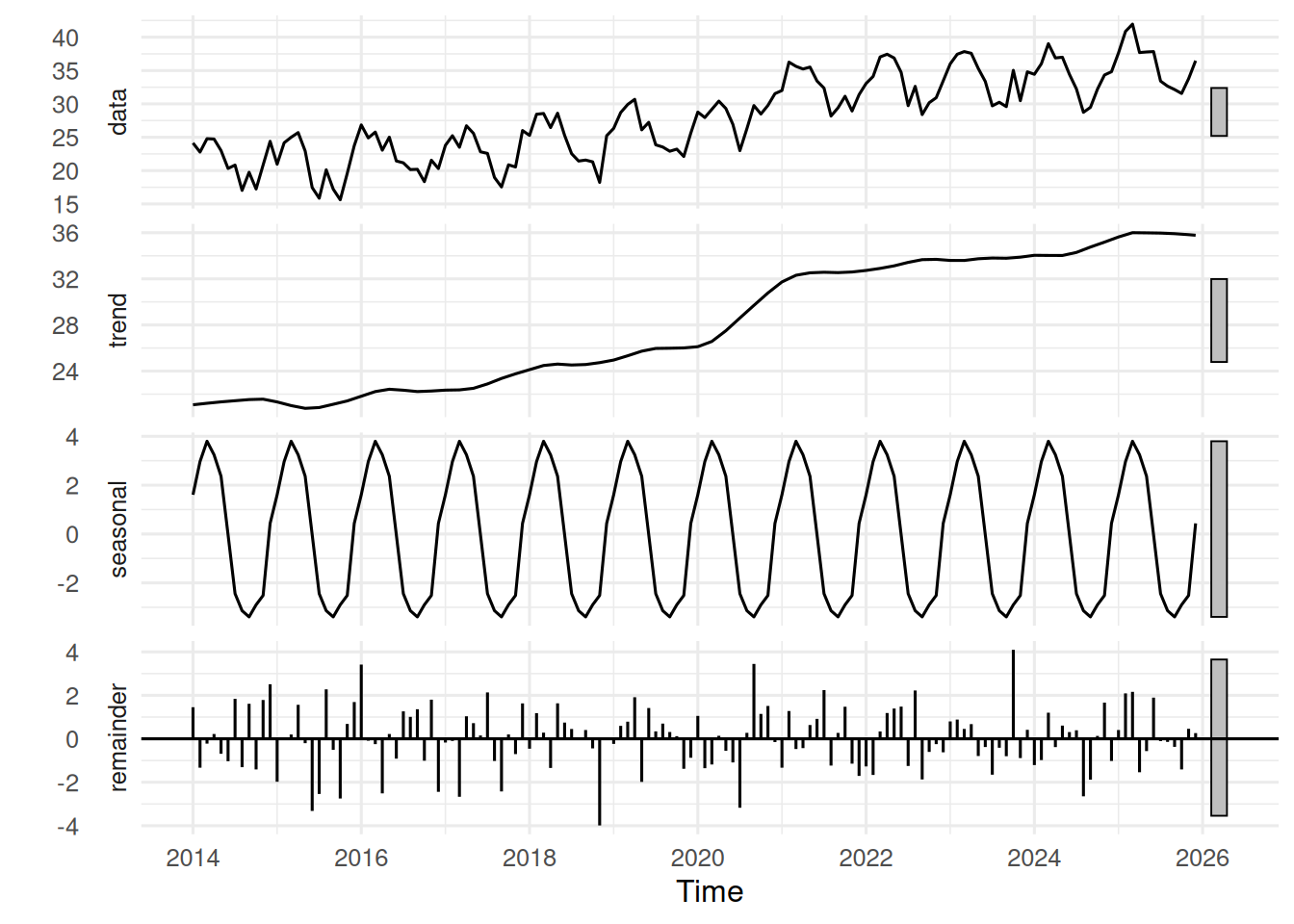

2. Visualise

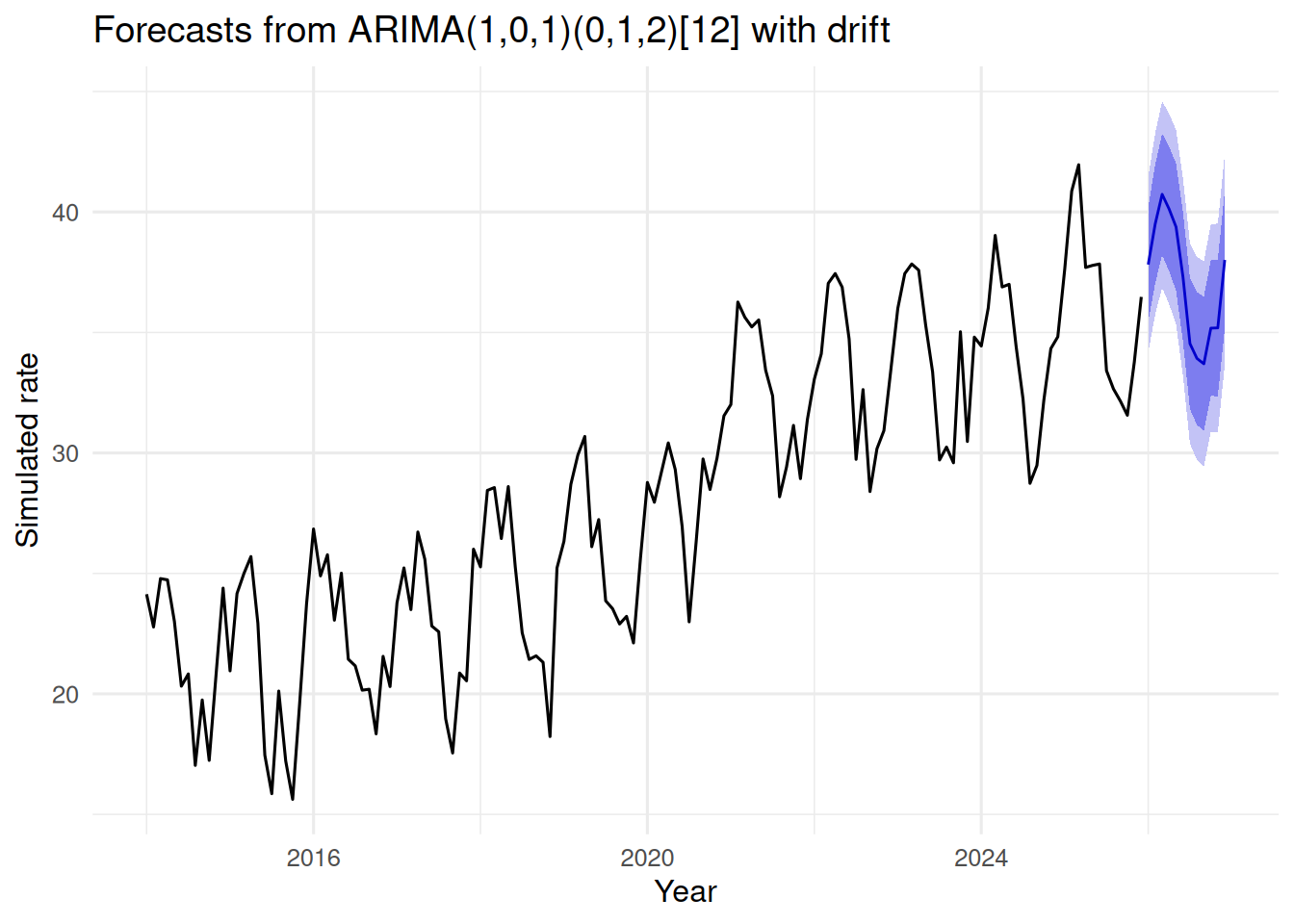

4. Conduct

Series: ts_y

ARIMA(3,0,0)(0,1,1)[12] with drift

Coefficients:

ar1 ar2 ar3 sma1 drift

0.2914 0.2103 0.1666 -0.8570 0.1238

s.e. 0.0862 0.0889 0.0874 0.1125 0.0114

sigma^2 = 3.51: log likelihood = -275.6

AIC=563.2 AICc=563.87 BIC=580.49

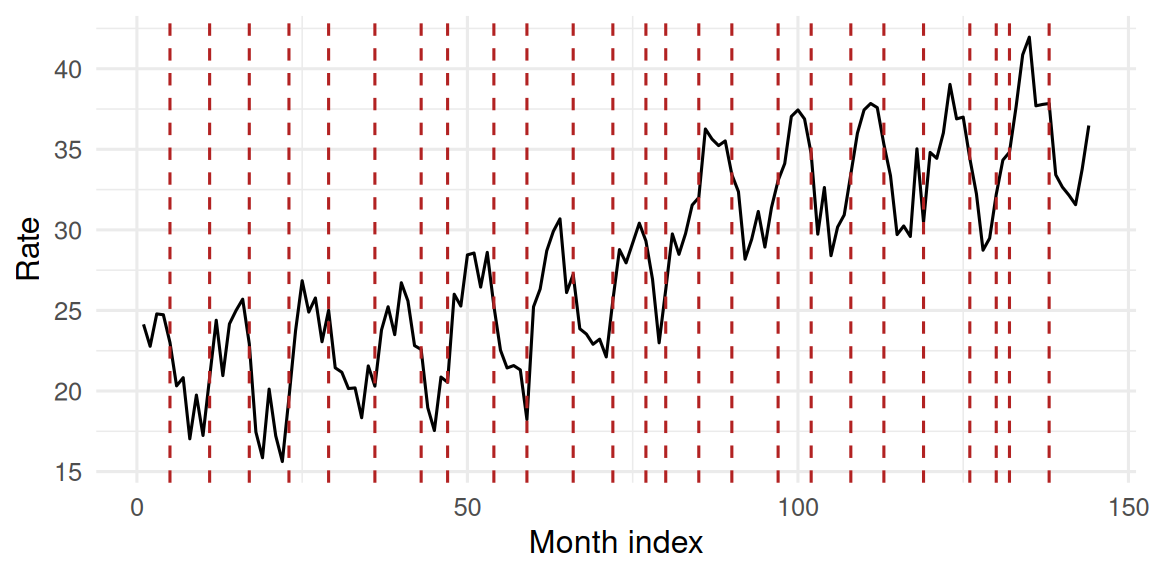

[1] 5 11 17 23 29 36 43 47 54 59 66 72 77 80 85 90 97 102 108

[20] 113 119 126 130 132 138